As someone who has long been invested in pioneering record management innovations, I find the intersection of blockchain and KYC (Know Your Customer) compliance to be particularly exciting. This convergence offers an evolved way of viewing compliance, where transformative technology turns traditionally cumbersome tasks into streamlined, efficient processes.

Why KYC Compliance Is Essential

Before diving into how blockchain technology enhances KYC processes, it’s important to understand why KYC compliance holds such significance for businesses, especially in finance. KYC protocols are designed to prevent fraud, money laundering, and terrorist financing by verifying the identity of clients—a necessity for both legal compliance and customer trust. However, the conventional approach is often fraught with inefficiencies, frequent errors, and significant costs.

The Problem with Traditional KYC Processes

Traditional systems of KYC compliance are labor-intensive and often lack the necessary flexibility to deal with modern challenges. From gathering diverse documents to maintain up-to-date records, these processes can be as frustrating as they are time-consuming. What many business leaders and compliance managers want is a solution that not only meets regulatory requirements but also improves operational efficiency. This is where blockchain technology truly shines.

Blockchain: A Game Changer for KYC

Blockchain technology offers a decentralized ledger that ensures data integrity, security, and transparency. Imagine having a tamper-proof method for verifying customer identities, where every update is recorded across all nodes in real-time, eliminating the need for manual reconciliation of records. This way, each transaction or update is validated and stored universally, saving both time and resources.

1. Data Integrity and Immutability

One of blockchain’s core strengths is its ability to provide a permanent and immutable record. Each data entry related to a customer’s identity is securely hashed on the blockchain, ensuring that it cannot be altered retroactively. This feature significantly reduces the risk of data breaches, providing an impressive layer of security that traditional systems lack.

2. Streamlined Process and Reduction of Duplication

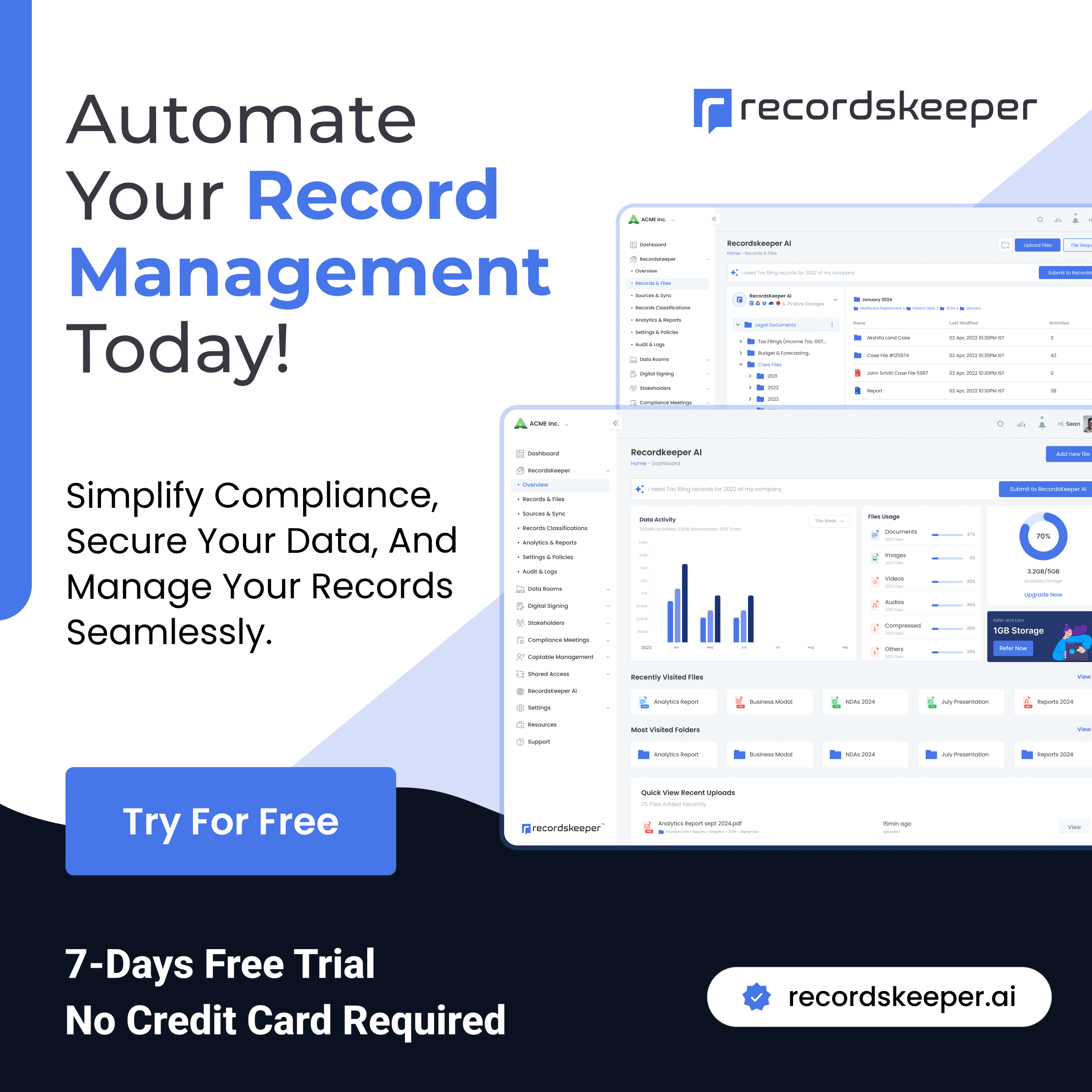

Since each participant on the blockchain network has access to real-time, verified data, it eliminates the need for repeated KYC procedures with different entities. Once a platform like RecordsKeeper.AI, which integrates blockchain technology, has conducted an identity verification, other organizations can access this verified information with the customer’s consent, simplifying processes, reducing paperwork, and lowering costs.

3. Improved Client Experience

An often-overlooked aspect of KYC compliance is the client experience. Nobody likes being asked to submit the same set of documents multiple times. By allowing businesses to share verified KYC data across a secure blockchain platform, customer interaction becomes less intrusive and more efficient, ultimately leading to higher customer satisfaction and retention.

4. Real-Time Monitoring

Blockchain enables real-time monitoring through smart contracts, automating alerts and notifications for suspicious activities. This helps businesses not just comply with regulations but also actively engage in crime prevention efforts. The audit trails generated provide comprehensive records that are easy to follow and demonstrate compliance effectively.

Implications for Compliance Officers and Heads of Record Management

If you’re in charge of compliance or record-keeping in your organization, adapting to blockchain-based KYC processes can bring numerous advantages. Not only does it ensure adherence to ever-evolving regulatory landscapes, but it also offers operational efficiency and enhanced security. The transition might seem daunting, but platforms like RecordsKeeper.AI are simplifying this shift by offering intuitive interfaces and comprehensive support.

By leveraging blockchain technology, organizations can effectively turn compliance from a task of mere obligation into a strategic business advantage.

Conclusion: The Path Forward

The essence of blockchain for KYC compliance lies in optimizing what we already know and improving it through innovative technology. As we move forward in this digital age, embracing blockchain isn’t just an option—it’s a necessity for those looking to secure their business’s foothold in tomorrow’s market. For those looking to dive deeper into how you can strategically implement blockchain in your compliance protocols, I invite you to explore more resources on our platform or reach out directly. Together, we can transform routine record management into a powerhouse of efficiency and security.

For more updates and insights about how we’re revolutionizing record management, follow along with me—Toshendra Sharma—on our journey at RecordsKeeper.AI.